Global RNA Therapeutics Market Size and Share Analysis 2026-2033

Global RNA Therapeutics Market Forecast Snapshot (2026???2033)

| Metric | Value |

|---|---|

| Market Size (2025) | USD 6.9 Billion |

| Market Size (2033) | USD 22.4 Billion |

| CAGR (2026???2033) | 15.8% |

| Largest Segment | siRNA Therapeutics |

| Fastest-Growing Segment | mRNA Therapeutics |

| Leading Application | Oncology |

| Fastest-Growing Application | Rare Genetic Disorders |

| Dominant Delivery Technology | Lipid Nanoparticle (LNP) Delivery Systems |

| Largest End User | Pharmaceutical & Biotechnology Companies |

| Dominant Region | North America |

| Fastest-Growing Region | Asia-Pacific |

| Key Growth Driver | Advancements in mRNA Technologies and Growing Demand for Precision Medicine |

Global RNA Therapeutics Market Size & Forecast

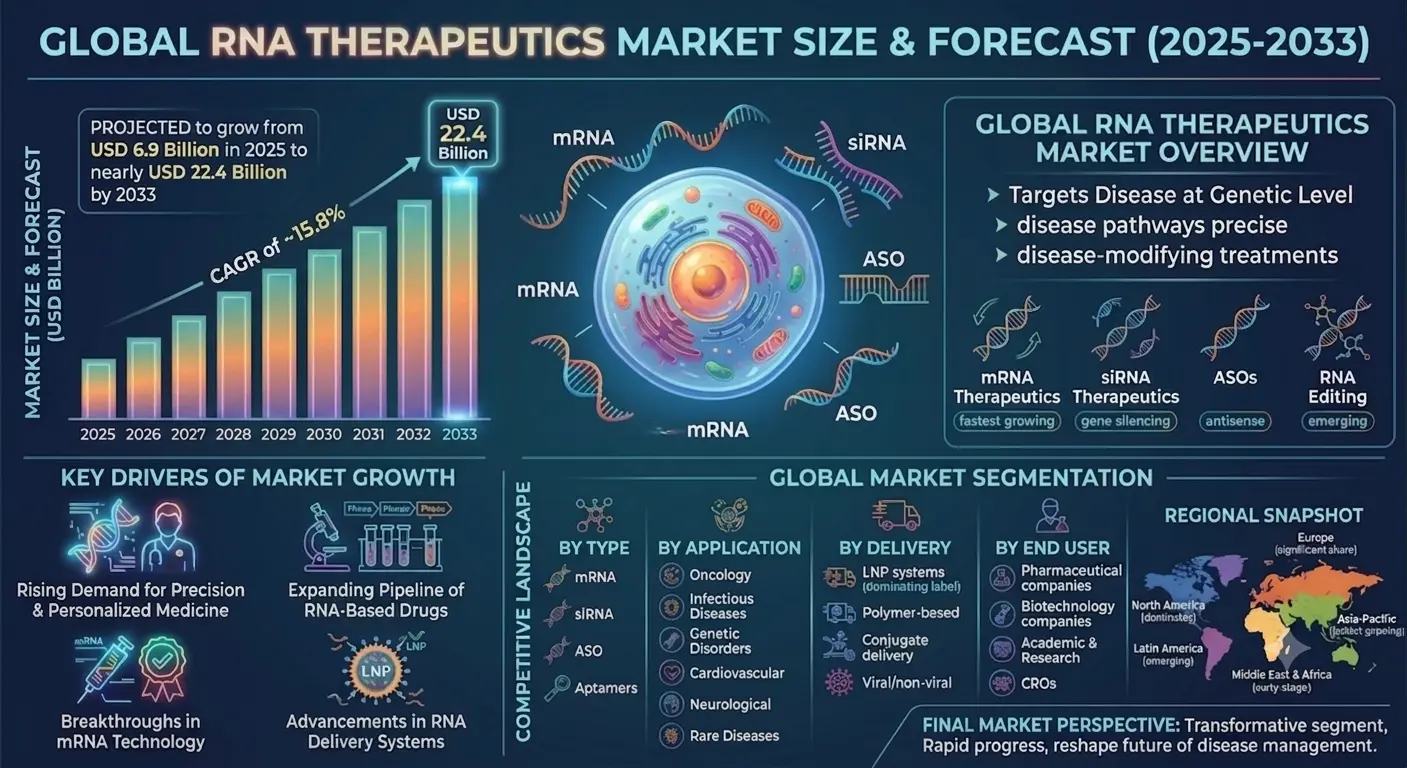

The global RNA therapeutics market is projected to witness rapid and transformative growth during the forecast period from 2026 to 2033. The market was valued at approximately USD 6.9 billion in 2025 and is expected to reach nearly USD 22.4 billion by 2033, expanding at a CAGR of around 15.8%. This strong growth is driven by breakthroughs in genetic medicine, rising prevalence of chronic and rare diseases, increasing adoption of precision medicine, and continuous advancements in RNA delivery technologies. RNA therapeutics represent a new generation of drug modalities that use ribonucleic acid (RNA) molecules to regulate gene expression, silence disease-causing genes, or produce therapeutic proteins. Key RNA-based technologies include mRNA therapeutics, small interfering RNA (siRNA), antisense oligonucleotides (ASOs), and RNA aptamers. The market has gained significant momentum following the success of mRNA vaccines, which demonstrated the scalability, speed, and clinical effectiveness of RNA-based platforms. This has accelerated investment and research across oncology, infectious diseases, cardiovascular disorders, neurological conditions, and rare genetic diseases. Increasing collaboration between biotechnology companies, pharmaceutical firms, and academic institutions is further accelerating innovation in RNA drug discovery and clinical development.Global RNA Therapeutics Market Overview

The RNA therapeutics market represents one of the most advanced and rapidly evolving segments of the global biopharmaceutical industry. Unlike traditional small-molecule drugs, RNA-based therapies target disease pathways at the genetic level, enabling highly precise and potentially disease-modifying treatments. The market includes multiple therapeutic platforms such as mRNA-based protein replacement therapies, siRNA drugs for gene silencing, antisense oligonucleotides for RNA modulation, and emerging RNA editing technologies. RNA therapeutics are increasingly being explored for diseases with limited or no existing treatment options, including rare genetic disorders, certain cancers, neurodegenerative diseases, and viral infections. Major industry participants include Moderna Inc., BioNTech SE, Alnylam Pharmaceuticals, Ionis Pharmaceuticals, Sarepta Therapeutics, Arcturus Therapeutics, CureVac, Dicerna Pharmaceuticals (Novo Nordisk company), and Arrowhead Pharmaceuticals. The market is heavily influenced by advancements in lipid nanoparticle (LNP) delivery systems, improved RNA stability technologies, and scalable manufacturing processes that support commercial viability.Key Drivers of Global RNA Therapeutics Market Growth

Rising Demand for Precision and Personalized Medicine

The shift toward precision medicine is driving strong demand for therapies that can target diseases at the genetic and molecular level. RNA therapeutics enable highly specific interventions tailored to individual patient profiles. This approach improves treatment efficacy while minimizing off-target effects, making RNA-based drugs highly attractive for complex disease management.Expanding Pipeline of RNA-Based Drugs

The global clinical pipeline for RNA therapeutics is expanding rapidly, with increasing numbers of candidates in preclinical, Phase I, II, and III trials across multiple therapeutic areas. Strong investment in biotech startups and pharmaceutical R&D is accelerating the development of next-generation RNA platforms.Breakthroughs in mRNA Technology

The success of mRNA vaccines has validated the commercial and clinical potential of RNA technologies. This has led to expanded research into mRNA-based therapies for cancer immunotherapy, protein replacement, and rare genetic diseases. Improved mRNA stability, optimized codon design, and enhanced delivery systems are further strengthening this segment.Advancements in RNA Delivery Systems

Efficient delivery of RNA molecules remains a critical factor for therapeutic success. Innovations in lipid nanoparticles, polymer-based carriers, and targeted delivery systems are significantly improving drug performance. These advancements are enabling safer, more effective, and more scalable RNA-based treatments.Rising Burden of Chronic and Rare Diseases

The increasing prevalence of cancer, cardiovascular diseases, neurological disorders, and rare genetic conditions is driving demand for novel therapeutic approaches. RNA therapeutics offer promising solutions for diseases that were previously considered untreatable or difficult to manage with conventional drugs.Global RNA Therapeutics Market Segmentation

By Type

The market is segmented into mRNA therapeutics, siRNA therapeutics, antisense oligonucleotides (ASOs), RNA aptamers, and others. mRNA therapeutics represent the fastest-growing segment due to expanding vaccine and protein replacement applications, while siRNA therapies are widely used for gene silencing applications.By Application

Applications include oncology, infectious diseases, genetic disorders, cardiovascular diseases, neurological disorders, and rare diseases. Oncology remains a key focus area due to the potential of RNA-based immunotherapies and tumor-targeted treatments.By Delivery Technology

The market includes lipid nanoparticle (LNP) delivery, polymer-based delivery, conjugate delivery systems, and viral/non-viral vectors. Lipid nanoparticle systems dominate due to their proven effectiveness in mRNA vaccine delivery and therapeutic applications.By End User

End users include pharmaceutical companies, biotechnology companies, academic and research institutes, and contract research organizations (CROs). Pharmaceutical and biotech companies account for the largest share due to high investment in RNA drug development and commercialization.Regional Market Dynamics

North America

North America dominates the RNA therapeutics market due to strong biotechnology infrastructure, high R&D investment, and early adoption of advanced therapies. The United States leads global innovation with major RNA-focused companies, robust funding ecosystems, and strong regulatory support for accelerated drug approvals.Europe

Europe holds a significant market share supported by strong pharmaceutical research capabilities, government funding for biotechnology, and expanding clinical trial activity. Countries such as Germany, Switzerland, the United Kingdom, and Belgium are key hubs for RNA research and development.Asia-Pacific

Asia-Pacific is the fastest-growing region due to increasing biotechnology investments, expanding clinical research infrastructure, and rising government support for life sciences innovation. China, Japan, and South Korea are leading contributors to regional growth in RNA therapeutics development and manufacturing.Latin America

Latin America is an emerging market driven by growing clinical research participation and gradual expansion of advanced healthcare infrastructure.Middle East & Africa

The region is witnessing early-stage adoption of advanced therapeutics, supported by increasing healthcare investments and international collaborations in biotechnology research.Competitive Landscape

The global RNA therapeutics market is highly innovative and competitive, dominated by biotechnology firms and leading pharmaceutical companies focused on genetic medicine. Key players include Moderna Inc., BioNTech SE, Alnylam Pharmaceuticals, Ionis Pharmaceuticals, Sarepta Therapeutics, Arcturus Therapeutics, CureVac, Dicerna Pharmaceuticals (Novo Nordisk), Arrowhead Pharmaceuticals, and Wave Life Sciences. Companies are heavily investing in RNA platform expansion, delivery technology innovation, and strategic collaborations to accelerate drug development pipelines. Mergers, licensing agreements, and research partnerships with academic institutions are common strategies to strengthen technological capabilities and market positioning.Strategic Outlook

The strategic outlook for the global RNA therapeutics market remains extremely strong due to its potential to redefine modern medicine through genetic-level intervention. Future growth opportunities include RNA-based oncology therapies, next-generation mRNA vaccines, RNA editing technologies, and combination therapies integrating RNA with immunotherapy and gene editing platforms. Advancements in scalable manufacturing, cold-chain optimization, and cost-efficient delivery systems will play a critical role in broader commercialization. Companies investing early in platform diversification, delivery innovation, and clinical pipeline expansion are expected to lead the next wave of biopharmaceutical breakthroughs.Final Market Perspective

The global RNA therapeutics market is positioned as one of the most transformative segments in modern biotechnology. Rapid technological progress, expanding clinical applications, and strong investment momentum are driving sustained market growth. As RNA-based therapies continue to evolve from experimental treatments to mainstream clinical solutions, the industry is expected to reshape the future of disease management across multiple therapeutic areas. Organizations that successfully integrate innovation, regulatory expertise, and scalable manufacturing capabilities will remain strongly positioned in this high-growth and scientifically advanced market.Table of Contents

Table of Contents

- 1. Executive Summary

- 1.1 Global RNA Therapeutics Market Snapshot (2026-2033)

- 1.2 Market Size & CAGR Analysis

- 1.3 Largest & Fastest-Growing Segments

- 1.4 Key Regional Insights

- 1.5 Major Market Growth Drivers

- 1.6 Competitive Landscape Overview

- 1.7 Strategic Outlook Through 2033

- 2. Introduction & Market Overview

- 2.1 Definition of RNA Therapeutics

- 2.2 Scope of the Study

- 2.3 Evolution of RNA-Based Drug Modalities

- 2.4 RNA Therapeutics Value Chain & Development Pipeline

- 2.5 RNA Modalities & Technology Platforms

- 2.6 Regulatory & Clinical Development Landscape

- 2.7 RNA Delivery System Innovations

- 3. Research Methodology

- 3.1 Primary Research

- 3.2 Secondary Research

- 3.3 Market Size Estimation Model

- 3.4 Forecast Assumptions (2026-2033)

- 3.5 Data Validation & Market Triangulation

- 4. Market Dynamics

- 4.1 Drivers

- 4.1.1 Rising Demand for Precision & Personalized Medicine

- 4.1.2 Expanding Pipeline of RNA-Based Drugs

- 4.1.3 Breakthroughs in mRNA Technology

- 4.1.4 Advancements in RNA Delivery Systems

- 4.1.5 Rising Burden of Chronic & Rare Diseases

- 4.2 Restraints

- 4.2.1 High Development & Manufacturing Costs

- 4.2.2 Stability & Storage Challenges of RNA Molecules

- 4.2.3 Regulatory Complexity for Novel Biologics

- 4.2.4 Limited Large-Scale Manufacturing Infrastructure

- 4.3 Opportunities

- 4.3.1 RNA-Based Oncology & Immunotherapy Expansion

- 4.3.2 Next-Generation mRNA Vaccines & Therapies

- 4.3.3 RNA Editing & Gene Regulation Technologies

- 4.3.4 Combination Therapies with Gene Editing Platforms

- 4.4 Challenges

- 4.4.1 Delivery Efficiency & Targeting Limitations

- 4.4.2 Cold Chain & Stability Constraints

- 4.4.3 High Competition in Biotech Innovation Space

- 4.4.4 Clinical Trial Complexity & Time-to-Market Delays

- 4.1 Drivers

- 5. Global RNA Therapeutics Market Analysis (USD Billion), 2026-2033

- 5.1 Market Size Overview

- 5.2 CAGR Analysis

- 5.3 Regional Revenue Distribution

- 5.4 Segment Revenue Analysis

- 5.5 Clinical Pipeline & Investment Trends

- 5.6 Technology Adoption & Commercialization Trends

- 6. Market Segmentation (USD Billion), 2026-2033

- 6.1 By Type

- 6.1.1 mRNA Therapeutics

- 6.1.1.1 Vaccine Applications

- 6.1.1.1.1 Protein Replacement Therapies

- 6.1.1.1.1.1 Oncology Immunotherapy Applications

- 6.1.1.1.1 Protein Replacement Therapies

- 6.1.1.1 Vaccine Applications

- 6.1.2 siRNA Therapeutics

- 6.1.2.1 Gene Silencing Applications

- 6.1.2.1.1 Targeted Disease Modulation

- 6.1.2.1.1.1 Rare Disease Treatments

- 6.1.2.1.1 Targeted Disease Modulation

- 6.1.2.1 Gene Silencing Applications

- 6.1.3 Antisense Oligonucleotides (ASOs)

- 6.1.3.1 RNA Modulation Therapies

- 6.1.4 RNA Aptamers

- 6.1.5 Others (RNA Editing & Emerging Platforms)

- 6.1.1 mRNA Therapeutics

- 6.2 By Application

- 6.2.1 Oncology

- 6.2.2 Infectious Diseases

- 6.2.3 Genetic Disorders

- 6.2.4 Cardiovascular Diseases

- 6.2.5 Neurological Disorders

- 6.2.6 Rare Diseases

- 6.3 By Delivery Technology

- 6.3.1 Lipid Nanoparticle (LNP) Delivery

- 6.3.2 Polymer-Based Delivery Systems

- 6.3.3 Conjugate Delivery Systems

- 6.3.4 Viral & Non-Viral Vectors

- 6.4 By End User

- 6.4.1 Pharmaceutical Companies

- 6.4.2 Biotechnology Companies

- 6.4.3 Academic & Research Institutes

- 6.4.4 Contract Research Organizations (CROs)

- 6.1 By Type

- 7. Market Segmentation by Geography

- 7.1 North America

- 7.2 Europe

- 7.3 Asia-Pacific

- 7.4 Latin America

- 7.5 Middle East & Africa

- 8. Competitive Landscape

- 8.1 Market Share Analysis

- 8.2 RNA Platform Technology Benchmarking

- 8.3 Clinical Pipeline Strength Analysis

- 8.4 Strategic Collaborations & Licensing Agreements

- 8.5 Manufacturing & Delivery Innovation Strategies

- 9. Company Profiles

- 9.1 Moderna Inc.

- 9.2 BioNTech SE

- 9.3 Alnylam Pharmaceuticals

- 9.4 Ionis Pharmaceuticals

- 9.5 Sarepta Therapeutics

- 9.6 Arcturus Therapeutics

- 9.7 CureVac

- 9.8 Dicerna Pharmaceuticals (Novo Nordisk)

- 9.9 Arrowhead Pharmaceuticals

- 9.10 Wave Life Sciences

- 10. Strategic Intelligence & Pheonix AI Insights

- 10.1 RNA Therapeutics Forecast Intelligence Engine

- 10.2 Clinical Trial Progress Tracker

- 10.3 RNA Delivery Optimization Analytics

- 10.4 Pipeline & Investment Mapping System

- 10.5 Automated Porter???s Five Forces Analysis

- 11. Future Outlook & Strategic Recommendations

- 11.1 Expansion of RNA-Based Oncology & Immunotherapy

- 11.2 Investment in Scalable RNA Manufacturing Platforms

- 11.3 Advancement of Next-Generation Delivery Systems

- 11.4 Integration with Gene Editing & Combination Therapies

- 11.5 Long-Term Market Outlook (2033+)

- 12. Appendix

- 13. About Pheonix Research

- 14. Disclaimer

Competitive Landscape

Global RNA Therapeutics Market Competitive Intensity & Market Structure Overview

The Global RNA Therapeutics Market is a highly innovation-driven and rapidly evolving segment of the biopharmaceutical industry, characterized by strong competition among biotechnology companies, pharmaceutical giants, and emerging RNA-focused startups. Competitive intensity is exceptionally high due to the scientific complexity of RNA-based drug development, high R&D costs, and the race to establish platform dominance in next-generation genetic medicine.

The market structure is currently oligopolistic at the top end, with a small group of leading biotech firms controlling most commercialized RNA therapies, while a broad ecosystem of emerging companies is engaged in early-stage pipeline development. Competition is primarily based on delivery technology, clinical pipeline strength, intellectual property ownership, and scalability of manufacturing platforms.

Strategic collaborations, licensing agreements, and acquisitions are central to market dynamics, as large pharmaceutical companies increasingly partner with RNA-specialized biotech firms to gain access to innovative technologies and accelerate drug development timelines.

Global RNA Therapeutics Market Competitive Intensity & Market Structure Current Scenario

Leading Biotechnology & Pharmaceutical Players

Moderna Inc.: A global leader in mRNA technology, widely recognized for its pioneering role in mRNA vaccines and expanding pipeline of infectious disease and oncology therapeutics.

BioNTech SE: A major mRNA innovation company focused on cancer immunotherapy and infectious disease vaccines, with strong collaboration networks across global pharma partners.

Alnylam Pharmaceuticals: A dominant player in siRNA therapeutics, specializing in gene-silencing treatments for rare and genetic diseases.

Ionis Pharmaceuticals: A leader in antisense oligonucleotide (ASO) technologies with a strong portfolio of neurological and rare disease therapies.

Sarepta Therapeutics: Focused on genetic medicine, particularly RNA-targeted therapies for rare neuromuscular disorders.

Arcturus Therapeutics: An emerging mRNA therapeutics company developing vaccines and liver-targeted RNA therapies.

CureVac: A pioneer in mRNA technology platforms, focusing on next-generation RNA design and improved stability systems.

Arrowhead Pharmaceuticals: Specializes in RNA interference (RNAi) therapies targeting chronic and metabolic diseases.

Dicerna Pharmaceuticals (Novo Nordisk): Strengthens the siRNA segment through metabolic disease-focused RNA therapeutics integrated into a global pharmaceutical network.

Wave Life Sciences: Focused on precision RNA medicines using stereopure oligonucleotide technology for rare diseases.

Major Pharmaceutical Collaborators: Pfizer, Roche, Novartis, and AstraZeneca are actively involved in RNA therapeutic development through partnerships, licensing deals, and co-development programs.

Key Competitive Intensity & Market Structure Signals in Global RNA Therapeutics Market

A major competitive signal in the market is the dominance of platform-based innovation, where companies compete not just on individual drugs but on proprietary RNA delivery systems, molecular engineering techniques, and scalable manufacturing technologies. Intellectual property ownership around lipid nanoparticle (LNP) delivery systems and RNA stabilization technologies remains a critical competitive barrier.

Another key factor shaping competition is the rapid expansion of clinical pipelines across oncology, rare diseases, and infectious diseases. Companies with diversified and late-stage clinical assets are gaining a significant advantage in attracting investment and forming strategic partnerships with large pharmaceutical players.

Manufacturing scalability and cold-chain logistics capabilities are emerging as important differentiators, particularly for mRNA-based therapeutics that require complex production and storage systems.

In addition, regulatory acceleration pathways for breakthrough therapies are intensifying competition, as companies race to achieve early approvals in high-value therapeutic segments such as cancer immunotherapy and genetic disorders.

Geographically, North America continues to dominate innovation and capital investment, while Europe and Asia-Pacific are rapidly expanding their roles in clinical research, manufacturing partnerships, and biotechnology infrastructure development.

Strategic Implications of Competitive Intensity & Market Structure in Global RNA Therapeutics Market

Companies are increasingly adopting platform-centric business models, focusing on scalable RNA technology platforms that can support multiple therapeutic applications rather than single-drug pipelines. This approach enhances long-term commercial potential and reduces development risk.

Strategic alliances between biotech innovators and large pharmaceutical companies are accelerating clinical development and global commercialization capabilities. These collaborations are essential for funding-intensive late-stage trials and regulatory approvals.

Investment in next-generation delivery systems, including lipid nanoparticles, polymer-based carriers, and targeted tissue delivery technologies, is becoming a central strategic priority to improve therapeutic efficacy and safety profiles.

The competitive landscape is also being shaped by increasing mergers and acquisitions, as larger pharmaceutical companies acquire RNA-focused startups to secure proprietary technologies and strengthen their genetic medicine portfolios.

Emerging markets are expected to play a growing role in clinical trials and manufacturing outsourcing, particularly in Asia-Pacific, where biotechnology ecosystems are rapidly expanding.

Global RNA Therapeutics Market Competitive Intensity & Market Structure Forward Outlook

The RNA therapeutics market is expected to become increasingly consolidated as leading players strengthen their platform dominance through acquisitions, licensing deals, and expanded clinical pipelines. However, continuous scientific innovation will ensure sustained entry of new biotech firms, maintaining a dynamic competitive environment.

Next-generation RNA modalities such as RNA editing, self-amplifying mRNA, and combination RNA-immunotherapy approaches are expected to redefine competitive boundaries in the coming years.

Manufacturing innovation, particularly in scalable RNA production and global distribution logistics, will become a key determinant of long-term market leadership.

Regulatory evolution supporting fast-track approvals for breakthrough genetic therapies will further intensify competition among leading players seeking early commercialization advantages.

Overall, the RNA therapeutics market will remain highly competitive but structurally progressive, driven by continuous innovation in genetic medicine. Companies that successfully integrate platform technology leadership, strong clinical pipelines, and scalable global manufacturing capabilities will remain dominant in the Global RNA Therapeutics Market through 2033.

Value Chain

Global RNA Therapeutics Market Value Chain & Supply Chain Evolution Overview

The Global RNA Therapeutics Market value chain is undergoing a major transformation from traditional pharmaceutical development models toward highly advanced, genetically targeted, technology-driven, and precision-focused biopharmaceutical ecosystems. This evolution is being driven by breakthroughs in mRNA technologies, increasing demand for precision medicine, expanding applications in oncology and rare diseases, rising investments in genetic medicine, and continuous advancements in RNA delivery systems and scalable manufacturing platforms.

The RNA therapeutics value chain begins with upstream research and raw material sourcing, which includes nucleotides, lipid nanoparticles (LNPs), enzymes, plasmid DNA templates, oligonucleotide intermediates, bioprocessing reagents, and specialized pharmaceutical-grade chemicals required for RNA synthesis and formulation. Suppliers of biotechnology materials, genomic reagents, synthetic biology components, and advanced delivery materials play a critical role in ensuring product quality, stability, and regulatory compliance. As RNA therapies require highly specialized ingredients and controlled production environments, companies are increasingly focusing on supplier diversification and long-term sourcing agreements to strengthen supply continuity.

The manufacturing layer forms the technological core of the RNA therapeutics value chain and includes RNA synthesis, oligonucleotide production, in vitro transcription processes, purification technologies, nanoparticle encapsulation, sterile filling operations, lyophilization, and advanced biologic processing systems. Pharmaceutical and biotechnology companies are heavily investing in automated manufacturing systems, AI-assisted quality monitoring, continuous bioprocessing technologies, and scalable RNA production infrastructure to improve efficiency, reduce production variability, and support large-scale commercialization. mRNA therapeutics and siRNA platforms are particularly driving demand for next-generation manufacturing technologies due to their rapid clinical expansion.

Contract development and manufacturing organizations (CDMOs) are becoming increasingly important within the RNA therapeutics ecosystem as biotechnology companies seek external expertise for process optimization, clinical-scale production, formulation development, and commercial manufacturing support. Specialized CDMOs with expertise in RNA synthesis, nanoparticle formulation, and biologics manufacturing are playing a critical role in accelerating clinical development timelines and improving scalability for emerging RNA-based therapies.

The distribution structure of the RNA therapeutics market is highly regulated and technologically sensitive, requiring specialized pharmaceutical logistics infrastructure, cold chain transportation systems, temperature-controlled storage facilities, and advanced tracking systems. RNA therapeutics often require ultra-low temperature handling and strict contamination control throughout transportation and storage operations. Distribution channels primarily involve pharmaceutical companies, specialty healthcare distributors, hospital networks, research institutions, and specialty pharmacies responsible for advanced therapeutic administration.

Regulatory compliance and quality assurance represent central pillars of the RNA therapeutics value chain. Manufacturers must comply with stringent standards established by organizations such as the U.S. FDA, European Medicines Agency (EMA), WHO, PMDA, and other national regulatory authorities governing Good Manufacturing Practices (GMP), biologics safety protocols, clinical validation requirements, and pharmacovigilance systems. Companies are increasingly investing in digital quality management systems, automated inspection technologies, and real-time manufacturing analytics to strengthen compliance and improve operational transparency.

Overall, the RNA therapeutics value chain is evolving into a highly sophisticated, innovation-intensive, digitally integrated, and globally interconnected biotechnology ecosystem focused on scalability, precision medicine, scientific advancement, and long-term therapeutic effectiveness.

Global RNA Therapeutics Market Value Chain & Supply Chain Evolution Current Scenario

The current RNA therapeutics supply chain is characterized by rapid technological advancement, increasing clinical commercialization, and growing global investment in advanced genetic medicine infrastructure. Biotechnology firms and pharmaceutical companies are aggressively expanding RNA research pipelines and manufacturing capabilities to support growing demand for mRNA therapeutics, siRNA therapies, antisense oligonucleotides, and emerging RNA editing technologies.

North America currently dominates the RNA therapeutics ecosystem due to strong biotechnology infrastructure, extensive R&D investment, and the presence of major RNA-focused pharmaceutical companies. Europe remains a major innovation hub supported by strong academic research institutions, biotechnology funding, and expanding clinical trial activity.

Asia-Pacific is rapidly emerging as a strategic manufacturing and research center for RNA therapeutics, particularly in China, Japan, and South Korea, where governments are increasing investments in biotechnology innovation, advanced biologics manufacturing, and genomic medicine infrastructure.

RNA manufacturing remains highly specialized and technically complex, with production processes requiring advanced purification systems, highly controlled cleanroom environments, and sophisticated encapsulation technologies. Supply chain bottlenecks related to lipid nanoparticles, specialized enzymes, and high-quality nucleic acid materials continue to influence production scalability across the industry.

Digital transformation is increasingly reshaping RNA therapeutics manufacturing operations through AI-assisted process optimization, predictive quality analytics, cloud-based manufacturing systems, digital twins, and automated bioprocess monitoring technologies. These systems are helping improve batch consistency, reduce manufacturing risks, and accelerate commercialization timelines.

At the same time, companies are increasingly focusing on strengthening cold chain logistics capabilities, regional manufacturing diversification, and strategic inventory management to improve supply chain resilience and reduce dependency on limited suppliers for critical biologic components.

Key Value Chain & Supply Chain Evolution Signals in Global RNA Therapeutics Market

One of the strongest transformation signals in the RNA therapeutics market is the rapid expansion of mRNA-based technologies beyond vaccines into oncology, rare diseases, protein replacement therapies, and personalized medicine applications. This shift is significantly expanding manufacturing infrastructure requirements and accelerating investment in advanced RNA production capabilities.

Another major evolution signal is the increasing importance of lipid nanoparticle (LNP) delivery technologies and targeted delivery systems. Efficient delivery remains one of the most critical technical challenges within RNA therapeutics, driving strong investment in next-generation encapsulation technologies, polymer-based carriers, and precision delivery platforms.

The growing role of CDMOs and strategic biotechnology partnerships is also reshaping the RNA therapeutics ecosystem. Pharmaceutical companies are increasingly relying on outsourcing partners to accelerate clinical development, optimize manufacturing scalability, and reduce commercialization risks.

Digitalization is becoming a defining characteristic of the RNA therapeutics value chain, with biotechnology firms adopting AI-powered drug discovery platforms, automated laboratory systems, real-time quality monitoring technologies, and cloud-based manufacturing analytics to improve research productivity and operational efficiency.

Supply chain resilience and regional diversification are also emerging as critical strategic priorities. Companies are increasingly investing in localized production capabilities, strategic raw material sourcing partnerships, and expanded cold-chain logistics networks to strengthen operational stability and reduce future disruption risks.

Strategic Implications of Value Chain & Supply Chain Evolution in Global RNA Therapeutics Market

The evolving RNA therapeutics value chain presents major strategic implications for biotechnology firms, pharmaceutical manufacturers, CDMOs, regulatory agencies, and healthcare providers. Companies that successfully combine advanced RNA platform technologies, scalable manufacturing infrastructure, and regulatory expertise are expected to strengthen their competitive positioning within the rapidly evolving genetic medicine landscape.

Investment in delivery technologies and biologics manufacturing infrastructure is becoming increasingly important as RNA therapies expand into broader therapeutic applications. Companies lacking advanced formulation capabilities or scalable production systems may face long-term commercialization limitations.

Supply chain resilience is becoming a strategic necessity as manufacturers seek to reduce dependency on limited suppliers for critical components such as lipid nanoparticles, nucleotides, and specialized biologic materials. Regional manufacturing expansion and supplier diversification are expected to become long-term operational priorities.

Digital transformation is creating significant competitive advantages within the RNA therapeutics ecosystem. AI-assisted drug discovery, automated bioprocessing systems, predictive manufacturing analytics, and intelligent quality control platforms are improving development speed, reducing operational costs, and strengthening regulatory compliance.

Long-term industry leadership will increasingly depend on a company???s ability to integrate scientific innovation, manufacturing scalability, regulatory excellence, cold-chain logistics capabilities, and strategic global partnerships within an increasingly competitive biotechnology environment.

Global RNA Therapeutics Market Value Chain & Supply Chain Evolution Forward Outlook

Between 2026 and 2033, the RNA therapeutics value chain is expected to become increasingly diversified, digitally integrated, automated, and commercially scalable as RNA-based therapies continue transitioning into mainstream clinical applications. Pharmaceutical and biotechnology companies are expected to continue expanding manufacturing infrastructure and investing in advanced RNA platform technologies to support rising global therapeutic demand.

mRNA therapeutics, siRNA drugs, RNA editing technologies, and personalized RNA medicines are expected to become major future growth segments, driving strong demand for next-generation bioprocessing systems, advanced delivery technologies, and specialized manufacturing facilities.

Continuous bioprocessing technologies, modular biologics manufacturing systems, and AI-driven production optimization platforms are expected to gain broader adoption due to their ability to improve scalability, reduce manufacturing complexity, and accelerate commercialization timelines.

Cold-chain optimization and decentralized manufacturing capabilities are expected to become increasingly important as companies seek to improve global accessibility and strengthen distribution efficiency for temperature-sensitive RNA therapies.

Sustainability and operational efficiency will also become increasingly important across the RNA therapeutics ecosystem, with manufacturers investing in energy-efficient biologics facilities, waste reduction technologies, and environmentally responsible production systems.

Ultimately, the future RNA therapeutics value chain will evolve into a highly intelligent, globally interconnected, and precision-focused biotechnology ecosystem where advanced manufacturing, delivery innovation, AI-assisted drug development, and resilient global supply networks collectively define long-term industry competitiveness.

Market-Specific Value Chain

- Raw Material & Biotechnology Input Supply: Nucleotide suppliers, lipid nanoparticle manufacturers, enzyme providers, plasmid DNA suppliers, biologic reagent companies

- RNA Synthesis & Therapeutic Manufacturing: mRNA production facilities, siRNA synthesis plants, oligonucleotide manufacturing units, biologics processing centers

- Delivery System & Formulation Development: Lipid nanoparticle developers, polymer-based delivery technology providers, encapsulation specialists, targeted delivery system companies

- Clinical Development & Contract Manufacturing: Biotechnology firms, pharmaceutical companies, CROs, CDMOs, clinical trial organizations

- Quality Assurance & Regulatory Compliance: GMP testing laboratories, biologics quality management systems, regulatory consulting providers, automated inspection technology companies

- Distribution & Cold Chain Logistics: Specialty pharmaceutical distributors, ultra-cold logistics providers, hospital supply chains, biologics warehousing operators

- Healthcare Integration & Therapeutic Administration: Hospitals, specialty clinics, oncology centers, genetic medicine providers, healthcare institutions

Investment Activity

Global RNA Therapeutics Market Investment & Funding Dynamics Overview

Investment and funding activity in the Global RNA Therapeutics Market is witnessing exceptional acceleration, driven by rapid advancements in genetic medicine, expanding clinical validation of RNA-based platforms, and rising venture capital interest in next-generation biotechnology. Between 2026 and 2033, funding is expected to remain strongly concentrated in mRNA therapeutics, siRNA platforms, antisense oligonucleotides (ASOs), and emerging RNA editing technologies, with increasing emphasis on scalable delivery systems and commercial manufacturing capabilities.

The market is evolving from early-stage scientific innovation into a commercially scalable biopharmaceutical ecosystem. This transition is attracting significant investments from venture capital firms, pharmaceutical giants, sovereign wealth funds, and strategic biotech investors. Companies such as Moderna Inc., BioNTech SE, Alnylam Pharmaceuticals, Ionis Pharmaceuticals, Sarepta Therapeutics, Arrowhead Pharmaceuticals, and Wave Life Sciences continue to receive substantial funding to expand clinical pipelines and strengthen RNA technology platforms.

A key driver of investment momentum is the proven success of mRNA-based vaccines, which validated RNA therapeutics as a commercially viable and rapidly deployable drug modality. This has led to increased capital allocation toward oncology RNA therapeutics, rare genetic disease treatments, infectious disease platforms, and next-generation personalized medicine approaches. Investors are particularly focused on companies that demonstrate strong intellectual property portfolios and proprietary RNA delivery technologies such as lipid nanoparticle (LNP) systems.

Additionally, strategic collaborations between pharmaceutical companies, biotechnology startups, and academic research institutions are playing a central role in funding innovation. Licensing agreements, milestone-based partnerships, and co-development deals are becoming key mechanisms for risk-sharing and accelerating clinical development timelines.

Global RNA Therapeutics Market Investment & Funding Dynamics Current Scenario

- North America: Leads global investment activity due to strong venture capital ecosystems, advanced biotech infrastructure, and high concentration of RNA-focused pharmaceutical companies in the United States.

- Europe: Witnessing significant funding growth supported by government-backed biotechnology initiatives, strong academic research institutions, and expanding clinical trial networks in Germany, Switzerland, and the United Kingdom.

- Asia-Pacific: Emerging as a high-growth investment region driven by increasing government support for life sciences, rising biotech startups, and expanding pharmaceutical manufacturing capabilities in China, Japan, and South Korea.

- Latin America & Middle East & Africa: Gradually attracting early-stage investments through clinical research participation, healthcare modernization initiatives, and international biotechnology collaborations.

Key Investment & Funding Dynamics Signals in Global RNA Therapeutics Market

- Rapid expansion of venture capital funding in mRNA and siRNA platform companies focused on oncology, rare diseases, and infectious diseases.

- Increasing pharmaceutical M&A activity targeting RNA technology startups with proprietary delivery systems and strong clinical pipelines.

- Rising investments in lipid nanoparticle (LNP) delivery technologies to improve RNA stability, targeting efficiency, and therapeutic scalability.

- Strong funding momentum in RNA-based oncology therapeutics due to high unmet clinical demand and large commercial potential.

- Growing interest in RNA manufacturing infrastructure, including scalable production facilities and cold-chain logistics systems.

- Expansion of public-private partnerships aimed at accelerating translational research and early-stage clinical trials.

- Increased funding for AI-driven drug discovery platforms integrated with RNA sequence design and therapeutic optimization.

Strategic Implications of Investment & Funding Dynamics in Global RNA Therapeutics Market

- The investment landscape is increasingly favoring platform-based RNA companies with multi-therapy pipelines rather than single-product biotech firms.

- Technological differentiation in RNA delivery systems is becoming a primary valuation driver for biotech startups.

- Strategic partnerships between pharmaceutical companies and biotech innovators are accelerating commercialization timelines and reducing development risks.

- Geographic diversification of R&D and manufacturing is becoming critical to mitigate supply chain risks and regulatory bottlenecks.

- Companies with strong clinical-stage pipelines and validated efficacy data are attracting premium valuations from institutional investors.

- Integration of AI, genomics, and RNA design technologies is emerging as a major investment theme shaping future drug discovery models.

- Long-term funding strategies are increasingly focused on scalable RNA platforms capable of addressing multiple disease indications.

Global RNA Therapeutics Market Investment & Funding Dynamics Forward Outlook

The Global RNA Therapeutics Market is expected to maintain strong and sustained investment momentum through 2033, supported by continuous clinical breakthroughs, expanding therapeutic applications, and growing acceptance of RNA-based medicine as a mainstream treatment modality.

Future funding activity will increasingly focus on next-generation RNA technologies, including self-amplifying mRNA platforms, RNA editing systems, targeted delivery mechanisms, and combination therapies integrating RNA with gene editing and immunotherapy approaches.

- North America: Will remain the dominant global investment hub, driven by strong biotech ecosystems and continued venture capital inflows.

- Europe: Will expand its role in early-stage research funding and regulatory-supported biotechnology innovation programs.

- Asia-Pacific: Will emerge as a major growth engine for both manufacturing investment and clinical research funding.

Overall, investment dynamics in the RNA therapeutics market will continue to be shaped by scientific innovation, regulatory advancements, and increasing commercialization success rates. Companies that successfully combine platform scalability, delivery innovation, and clinical validation are expected to attract the highest levels of funding and strategic investment interest throughout the forecast period.

Technology & Innovation

Global RNA Therapeutics Market Technology & Innovation Landscape Overview

The technology and innovation landscape of the Global RNA Therapeutics Market is evolving rapidly as biotechnology companies, pharmaceutical firms, and research institutions increasingly focus on gene-level intervention technologies. Innovation in this market is primarily driven by mRNA platforms, siRNA therapeutics, antisense oligonucleotides (ASOs), RNA aptamers, and next-generation RNA delivery systems designed to treat complex and previously untreatable diseases.

A major transformation in the market is being driven by advancements in RNA engineering, molecular biology, and genetic sequencing technologies. These developments are enabling precise control over gene expression, protein synthesis, and disease pathway modulation. As a result, RNA therapeutics are becoming a central pillar of precision medicine and personalized healthcare strategies worldwide.

One of the most significant innovation areas is RNA delivery technology. Since RNA molecules are inherently unstable, advanced delivery systems such as lipid nanoparticles (LNPs), polymer-based carriers, and ligand-targeted conjugates are being developed to ensure safe, efficient, and targeted delivery to specific tissues and cells. These systems have significantly improved clinical viability and scalability of RNA-based drugs.

Artificial intelligence and computational biology are also playing an increasingly important role in RNA drug discovery. AI-driven platforms are being used to design optimized RNA sequences, predict molecular interactions, and accelerate preclinical development timelines. This is significantly reducing research costs and improving success rates in clinical trials.

In addition, continuous advancements in mRNA synthesis, codon optimization, self-amplifying RNA (saRNA), and chemically modified nucleotides are enhancing stability, efficacy, and therapeutic durability of RNA-based treatments. These innovations are expanding applications beyond vaccines into oncology, rare genetic disorders, and chronic disease management.

Global RNA Therapeutics Market Technology & Innovation Landscape Current Scenario

Currently, the global RNA therapeutics market is experiencing rapid expansion as pharmaceutical companies increasingly shift toward genetic and molecular-level treatment approaches. North America and Europe dominate innovation activities due to strong biotech ecosystems, advanced research infrastructure, and high investment in genomic medicine.

The success of mRNA vaccines has significantly accelerated commercial and scientific interest in RNA platforms. This has led to increased funding for RNA-based oncology therapies, rare disease treatments, and infectious disease programs. Pharmaceutical companies are actively expanding their RNA pipelines through internal R&D and strategic collaborations with biotech startups.

RNA delivery remains one of the most active innovation areas, with lipid nanoparticle technology emerging as the most widely adopted system for clinical applications. Researchers are also exploring next-generation delivery methods such as exosome-based carriers and tissue-specific targeting ligands to improve precision and reduce side effects.

Manufacturing innovation is another key focus area. Scalable RNA synthesis, automated production systems, and improved cold-chain logistics are enabling faster commercialization of RNA therapeutics. These advancements are critical for supporting large-scale deployment of RNA-based drugs globally.

AI-powered drug discovery platforms are increasingly being used to analyze genetic datasets, identify therapeutic targets, and optimize RNA molecule design. This integration of computational tools with biotechnology is accelerating the development lifecycle of new RNA therapies.

Regulatory frameworks are also evolving to accommodate the rapid growth of RNA therapeutics. Agencies are introducing accelerated approval pathways for breakthrough RNA-based treatments, particularly in oncology and rare diseases, further supporting market expansion.

Key Technology & Innovation Trends in Global RNA Therapeutics Market

- mRNA Platform Expansion: Rapid development of mRNA-based vaccines, cancer immunotherapies, and protein replacement therapies.

- siRNA Gene Silencing Technologies: Targeted suppression of disease-causing genes for chronic and rare conditions.

- Advanced RNA Delivery Systems: Lipid nanoparticles, polymer carriers, and ligand-targeted delivery platforms improving cellular uptake.

- AI-Driven Drug Discovery: Machine learning models optimizing RNA sequence design and accelerating therapeutic development.

- Self-Amplifying RNA (saRNA): Next-generation RNA systems enabling lower dosage requirements and longer-lasting effects.

- RNA Stability Engineering: Chemical modifications improving RNA durability and reducing degradation in biological environments.

- Personalized RNA Medicine: Tailored RNA therapies based on individual genetic and molecular profiles.

- Scalable Manufacturing Technologies: Automated RNA synthesis and improved production systems enabling commercial-scale deployment.

- RNA Editing Technologies: Emerging platforms enabling precise correction of genetic mutations at RNA level.

- Combination Therapies: Integration of RNA therapeutics with immunotherapy, gene editing, and biologic drugs for enhanced efficacy.

Strategic Implications of Technology & Innovation

Technological innovation is fundamentally transforming the RNA therapeutics market by enabling highly precise, scalable, and adaptable treatment solutions. The convergence of molecular biology, computational science, and nanotechnology is creating a powerful ecosystem for next-generation drug development.

Pharmaceutical and biotechnology companies are increasingly investing in RNA platform technologies to diversify their therapeutic pipelines and address unmet medical needs. Strategic collaborations, licensing agreements, and joint research initiatives are becoming central to accelerating innovation.

Advancements in RNA delivery and stability technologies are significantly reducing clinical development risks and improving commercialization potential. Companies that can optimize delivery efficiency and manufacturing scalability are gaining strong competitive advantages.

At the same time, high development costs, regulatory complexities, cold-chain requirements, and technological barriers in large-scale production remain key challenges. Continuous investment in infrastructure and innovation is required to overcome these limitations.

Global RNA Therapeutics Market Technology & Innovation Forward Outlook

Looking ahead, the RNA therapeutics market is expected to evolve into a highly advanced precision medicine ecosystem driven by AI-enabled drug design, next-generation RNA platforms, and fully integrated genomic medicine solutions.

Future innovations are expected to focus on RNA editing technologies, multi-target RNA therapies, and fully personalized treatment approaches based on patient-specific genetic data. These advancements will significantly expand the scope of treatable diseases.

The integration of AI, genomics, and nanotechnology will further accelerate drug discovery and improve success rates in clinical development. This convergence is expected to redefine how complex diseases are treated at the molecular level.

Manufacturing innovation will also play a critical role, with scalable RNA production systems, automated synthesis platforms, and advanced formulation technologies enabling global accessibility of RNA-based treatments.

In conclusion, the Global RNA Therapeutics Market is undergoing a major technological transformation driven by genetic medicine, AI-powered discovery systems, and advanced delivery technologies. Companies that successfully integrate innovation, scalability, and precision medicine capabilities will lead the future of RNA-based healthcare solutions.

Market Risk

Global RNA Therapeutics Market Risk Factors & Disruption Threats Overview

The global RNA therapeutics market is experiencing strong growth driven by breakthroughs in genetic medicine, rising adoption of precision therapies, and expanding clinical applications across oncology, rare diseases, and infectious disorders. However, despite its transformative potential, the market remains highly complex and exposed to scientific, regulatory, manufacturing, financial, and geopolitical risks. As RNA-based drugs rely on advanced molecular engineering and sophisticated delivery systems, the industry faces elevated development uncertainty compared to conventional pharmaceutical modalities.

One of the primary risk factors in the RNA therapeutics market is the high clinical and regulatory failure rate associated with novel genetic therapies. RNA-based drugs require extensive validation for safety, efficacy, immune response management, and off-target effects. Regulatory agencies such as the FDA and EMA apply strict evaluation standards, and any unexpected toxicity or instability issues during trials can significantly delay or terminate development programs, leading to substantial financial losses for developers.

Manufacturing complexity and scalability constraints also represent major challenges. RNA therapeutics require highly controlled production environments, specialized synthesis technologies, and advanced purification processes. Scaling laboratory-grade RNA production to commercial volumes while maintaining quality consistency remains a significant bottleneck. Limited manufacturing capacity can restrict supply availability and delay commercialization timelines.

Delivery system limitations are another critical risk factor. RNA molecules are inherently unstable and require advanced delivery mechanisms such as lipid nanoparticles (LNPs) or polymer-based carriers. However, these systems can trigger immune responses, exhibit tissue delivery limitations, or face degradation issues in vivo. Inefficient delivery continues to be a major barrier to achieving consistent therapeutic outcomes across different disease indications.

High development costs and long commercialization timelines further increase financial risk in the RNA therapeutics market. The combination of intensive R&D investment, complex clinical trials, and specialized manufacturing infrastructure creates significant capital requirements. Smaller biotechnology firms often rely heavily on external funding, making them vulnerable to market downturns or reduced investor confidence.

Global RNA Therapeutics Market Risk Factors & Disruption Threats Current Scenario

The current RNA therapeutics market is characterized by rapid scientific innovation alongside increasing competitive pressure and regulatory scrutiny. Following the success of mRNA vaccines, there has been a surge in investment and pipeline expansion across RNA-based platforms. However, this rapid expansion has also intensified competition, leading to crowded development pipelines and higher pressure on clinical differentiation.

At present, supply chain dependencies for critical raw materials such as nucleotides, enzymes, lipid components, and specialized reagents are creating operational vulnerabilities. Any disruption in the global supply chain can impact production timelines and increase manufacturing costs, particularly for large-scale RNA vaccine and therapeutic production.

Regulatory uncertainty remains a significant concern as RNA therapeutics expand into new indications beyond vaccines. Evolving regulatory frameworks for gene-based medicines require continuous adaptation by developers, and differences in approval pathways across global regions can delay market entry strategies.

Intellectual property (IP) competition is also intensifying, with multiple companies developing overlapping RNA platforms, delivery technologies, and sequence designs. Patent disputes and licensing restrictions may limit market access or increase royalty burdens for emerging players.

In addition, increasing investor expectations following early mRNA successes are placing pressure on biotech companies to demonstrate rapid clinical outcomes. This can lead to accelerated development timelines that may increase clinical risk exposure and compromise long-term program stability.

Global RNA Therapeutics Market Key Risk Factors & Disruption Threat Signals

One of the most significant disruption signals in the RNA therapeutics market is the growing shift toward next-generation gene editing technologies such as CRISPR-based systems, which may compete with or complement RNA-based approaches. This technological convergence may reshape investment priorities and competitive positioning across the genetic medicine landscape.

Another key risk signal is the increasing complexity of clinical trial design for multi-target and combination RNA therapies. As treatments become more personalized, trial populations become smaller and more difficult to recruit, increasing the time and cost required for validation.

Cold-chain and ultra-low temperature storage requirements for certain RNA products, particularly mRNA-based formulations, continue to present logistical challenges. Any weaknesses in storage infrastructure or transportation networks can affect product stability and global distribution efficiency.

Immune system variability among patient populations represents another uncertainty factor, as RNA therapeutics may produce different responses depending on genetic background, comorbidities, and prior exposure to similar treatments. This variability complicates standardized treatment protocols.

Geopolitical and trade restrictions affecting biotechnology materials, intellectual property rights, and cross-border clinical collaboration may also disrupt global development and commercialization strategies.

Global RNA Therapeutics Market Strategic Implications of Risk Factors

Companies operating in the RNA therapeutics market must prioritize investment in advanced delivery technologies, scalable manufacturing platforms, and robust quality control systems to mitigate production and stability risks. Strengthening lipid nanoparticle innovation and alternative delivery mechanisms will remain a key competitive necessity.

Diversification of clinical pipelines across multiple RNA modalities, including mRNA, siRNA, and antisense oligonucleotides, can help reduce dependency on a single technology platform and balance development risk.

Strategic partnerships between biotechnology firms, pharmaceutical companies, and academic research institutions are increasingly important for sharing development costs, accessing specialized expertise, and accelerating clinical validation timelines.

Strengthening intellectual property strategies and securing global licensing agreements will be critical for protecting innovation and ensuring long-term commercial viability in a highly competitive environment.

Additionally, companies must invest in regulatory intelligence capabilities to navigate evolving global approval frameworks and ensure alignment with region-specific compliance requirements.

Global RNA Therapeutics Market Forward Risk Outlook

Looking ahead to 2026???2033, the RNA therapeutics market is expected to continue expanding rapidly, supported by advances in genetic medicine, expanding therapeutic applications, and increased investment in precision healthcare. However, the long-term outlook will remain shaped by technological uncertainty, regulatory evolution, manufacturing scalability, and competitive disruption from alternative gene-editing platforms.

Future risk dynamics will increasingly be influenced by the success or failure of late-stage clinical pipelines, improvements in RNA delivery efficiency, and the ability to scale cost-effective production systems globally. Companies that successfully overcome delivery, stability, and manufacturing challenges are likely to achieve significant competitive advantage.

Overall, while RNA therapeutics represent one of the most promising frontiers in modern medicine, the market will continue to require high levels of scientific innovation, regulatory adaptability, and financial resilience to navigate its complex and rapidly evolving risk landscape.

Regulatory Landscape

Global RNA Therapeutics Market Regulatory & Policy Environment Overview

The regulatory and policy environment governing the global RNA therapeutics market is highly complex, science-intensive, and rapidly evolving due to the novel nature of RNA-based drug modalities. RNA therapeutics, including mRNA, siRNA, antisense oligonucleotides (ASOs), and RNA aptamers, are regulated under advanced biologics and genetic medicine frameworks, requiring rigorous evaluation of safety, efficacy, manufacturing consistency, and long-term biological impact.

Regulatory agencies worldwide are continuously updating their frameworks to accommodate the rapid advancement of RNA-based technologies, particularly following the success of mRNA vaccines. These updates focus on accelerated approval pathways, enhanced clinical trial monitoring, manufacturing validation standards, and post-market surveillance for genetically active therapeutics.

In addition, RNA therapeutics introduce unique regulatory considerations related to delivery systems, such as lipid nanoparticles, immunogenicity risks, off-target gene effects, and long-term genetic expression control. As a result, regulatory oversight is significantly more stringent compared to traditional small-molecule drugs.

Global RNA Therapeutics Market Regulatory & Policy Environment Current Scenario

The current regulatory landscape for RNA therapeutics is characterized by fast-track approval mechanisms, conditional authorizations, and adaptive clinical trial designs, particularly for urgent therapeutic areas such as infectious diseases and oncology. Regulatory bodies are balancing rapid innovation with strict safety validation requirements.

In North America, the U.S. Food and Drug Administration (FDA) plays a leading role in regulating RNA therapeutics through biologics licensing frameworks, Investigational New Drug (IND) applications, and accelerated approval programs. The FDA has introduced emergency use authorizations and priority review pathways for RNA-based vaccines and therapies.

In Europe, the European Medicines Agency (EMA) regulates RNA therapeutics under advanced therapy medicinal product (ATMP) guidelines and stringent pharmacovigilance systems. Emphasis is placed on long-term safety monitoring, manufacturing quality consistency, and risk management plans for genetically active compounds.

Asia-Pacific regulatory bodies, including Japan???s PMDA and China???s NMPA, are actively expanding frameworks for RNA-based drug approvals. These regions are increasing investment in biotechnology regulation modernization, clinical trial infrastructure, and fast-track approval systems to support domestic innovation.

Latin America, the Middle East, and Africa are gradually aligning with international regulatory standards, primarily focusing on clinical trial participation, import approvals for advanced therapies, and capacity building for biologics oversight.

Key Regulatory & Policy Environment Signals in Global RNA Therapeutics Market

- Biologics & Advanced Therapy Classification: RNA therapeutics are regulated under biologics and advanced therapy frameworks requiring extensive safety, immunogenicity, and molecular validation.

- Accelerated Approval Pathways: Fast-track, breakthrough therapy, and conditional approval mechanisms are widely used to speed up access to RNA-based medicines.

- Clinical Trial Design & Oversight: Adaptive trial designs, real-world evidence integration, and expanded patient monitoring are increasingly required for RNA drug development.

- Manufacturing & Quality Control Standards: Strict GMP compliance, RNA sequence validation, lipid nanoparticle formulation control, and batch consistency are essential regulatory requirements.

- Pharmacovigilance & Long-Term Safety Monitoring: Continuous post-market surveillance is required to monitor immune responses, genetic interactions, and long-term therapeutic effects.

- Gene-Level Safety & Off-Target Effect Regulations: Regulatory agencies require detailed assessment of gene expression risks, off-target binding, and unintended biological impacts.

Strategic Implications of Regulatory & Policy Environment

The evolving regulatory framework is significantly shaping the development strategies of RNA therapeutics companies. Firms are increasingly investing in regulatory science capabilities, early-stage compliance planning, and integrated clinical development strategies to accelerate approval timelines.

Manufacturing scalability is a major regulatory focus area, particularly for mRNA and siRNA therapies, where consistency of RNA synthesis, purification, and delivery system integration must meet strict global standards. Companies are adopting advanced bioprocessing technologies and automated quality control systems to comply with these requirements.

The importance of delivery systems, especially lipid nanoparticles, has led regulators to closely evaluate formulation stability, biodistribution, and immunological safety, influencing how companies design their therapeutic platforms.

Regulatory emphasis on long-term monitoring is encouraging companies to build robust pharmacovigilance systems supported by real-world data analytics, patient registries, and AI-driven safety tracking tools.

Global harmonization efforts are also influencing strategy, as organizations such as the International Council for Harmonisation (ICH) work toward unified standards for gene-based and RNA-based therapies, reducing cross-border regulatory fragmentation.

Global RNA Therapeutics Market Regulatory & Policy Environment Forward Outlook

Between 2026 and 2033, the regulatory environment for RNA therapeutics is expected to become more structured, globally harmonized, and technology-integrated. Regulatory agencies will likely establish dedicated frameworks specifically tailored to RNA-based modalities, including standardized guidelines for mRNA vaccines, RNA editing therapies, and combination gene therapies.

Accelerated approval mechanisms are expected to expand further, particularly for high-unmet-need diseases such as cancer, rare genetic disorders, and neurodegenerative conditions. However, these faster pathways will be balanced by stricter post-market surveillance requirements.

Advancements in RNA delivery technologies and personalized medicine approaches will drive regulators to develop new evaluation models focusing on individualized treatment efficacy, biomarker-based approval systems, and adaptive regulatory frameworks.

International collaboration between regulatory authorities is expected to increase, improving consistency in clinical trial approvals, manufacturing standards, and pharmacovigilance systems across regions.

Overall, the regulatory and policy environment will remain a critical determinant of innovation speed, commercialization success, and global accessibility in the RNA therapeutics market. Companies that align early with evolving regulatory expectations, invest in compliance infrastructure, and build robust safety validation systems will be best positioned to lead in this rapidly advancing biotechnology sector.